The 411 On Points-Based Employee Recognition Programs

By Sean Mayo

Points-based employee recognition programs are designed to reward employees with tangible monetary awards while removing the negatives associated with cash.

With these types of programs, employees can earn and accumulate points in their personal point bank, giving them the flexibility to choose a reward that is perfect for them. Making employees feel valued and appreciated for their contributions is your first step to elevating employee engagement levels within your organization.

So, let’s dive into points-based reward systems and explain when they are used, how they are used, and how they impact your organization, both from a business outcome and a tax implication perspective.

Types of Employee Rewards and When to Use Them

According to a study titled “Incentives, Motivation and Workplace Performance: Research and Best Practices” by the Incentive Research Foundation (IRF) incentive reward programs can boost employee performance between 25-44%.

Non-monetary rewards are used to recognize an employee’s special achievement or the completion of something that enhances their job performance or value to the organization. Non-monetary awards are best used for:

- Peer-to-peer recognition

- Celebrating life events

- Showing appreciation

- Reinforcing good behavior or habits

Monetary rewards are cash bonuses, points, commissions, profit sharing, stock options used to recognize employees for exceptional performance or attainment of goals. Monetary rewards have instant monetary value and are generally used for:

- Commemorating service anniversaries

- Rewarding outstanding job performance

- Celebrating above and beyond service

- Nominations

Cash rewards are an option within monetary rewards. But there are many drawbacks to cash rewards, including the fact that the IRS requires that cash be treated as 100% taxable income by an employee. Plus, the company must cover its share of tax with workers' compensation and unemployment costs.

As an example, a $50 award will actually cost the company $73.79 and the employee will have only gotten $37.18 in buying power after taxes. To give the employee the full intended amount, the employer must include additional funds, which obviously impacts the budget.

Putting tax reasons aside for the moment, using cash as a reward equates to compensation. If someone is given a lump sum in cash, they're probably going to do something fairly sensible with it like spend it on groceries or put it straight into their savings account. Unfortunately, these actions remove the emotional attachment to the reward. Once cash is used, it’s gone — the employee has no memento or reminder of their effort or show to others.

The University of Chicago conducted a study seeking to improve the work speed and accuracy of their staff. Participants were offered cash, non-cash and verbal rewards.

The group that received cash performed 14.6% better than the group that received verbal praise. And the group that received non-cash rewards (messages or tangible rewards) performed 38.6% better than the group that received praise.

So, people like cash more than they like praise. But they like non-cash rewards at least twice as much as they like cash!

Non-cash rewards counterpunch many of the drawbacks of cash rewards, the first of which is increased motivation and performance. In an experiment by the Incentive Research Foundation (IRF), people who were incentivized with tangible rewards thought of them more frequently than those incentivized with cash, creating an emotional attachment that leads to better performance. When people find a reward more psychologically attractive, they want it more, so they are motivated to work harder to get it. And the benefits extend even further.

Favorable Tax Implications

- While sales tax is applicable in non-cash rewards, in a qualified plan most do not incur the same tax and fee obligations as a cash reward

- For the employer: Gift rewards are deductible as a business expense

- For the employee: There is no income tax liability for a gift item reward in a qualified plan

Higher Perceived Value

- Non-cash rewards offer a tangible item that the employee is more likely to keep as a reminder of their actions, increasing the likelihood they will repeat those actions

- A gift item is less likely to equate to compensation, making it more valuable, personal and giving it long-term meaning

More Memorable

- Employees will think of your company every time they recall the non-cash reward and positively associate that reward with their employer

- Employees can share their non-cash reward recognition with team, providing visibility that prompts others to do the same, for the same result

All About the Budget(ing)

Managing your Budget

A centralized budget is just that — centered in one location at a corporate level, managed and administered by one team, and shared amongst the various budget holders within an organization. The benefits of this are:

- There is reward equity across the entire company with all employees being treated equally and fairly, dollar for dollar

- Inconsistencies in program management that lead to inequity and dollar loss are virtually eliminated

- Budgeting and tracking are simplified — employees across multiple divisions are not inputting redundant information

- Big picture vision — spend is in one area, making controlling costs and corporate-wide decision-making easier

With decentralized budget management, a separate budget is allocated to each budget holder based on a committee decision. They are responsible for being accountable to the central accounting department and managing their own programs, budgets, and funding. The drawbacks of this type of budgeting are:

- When points are redeemed, they immediately hit the central accounting department for payment, even if the different budget holders have not yet reconciled

- Multiple budget holders managing multiple programs nets inconsistent payment procedures that could be a liability

- Multiple budget holders responsible for budgeting and submitting payments to the central accounting department make the program difficult to track and reconcile efficiently

- Employees may experience an unequal distribution of rewards… some employees may receive no rewards whereas others in different areas may receive many

Setting a Budget

Fixed budgets set a dollar amount for the program during a specified period of time, usually one year. The business rules of the program are then designed to stay within the confines of that budget. Fixed budgets give only finite control over spend because budget holders may use their budget too soon or run out, missing opportunities for recognition later in the period. On the flip side, they may “sandbag” their spending until the end of the period, missing critical recognition opportunities early on — and once the budget is gone, further recognition is not available.

Variable budgets are set based on desired outcomes and vary according to performance achieved. These budgets are usually determined by financially defining the outcomes they seek from their employees and what setting what they are “worth” to the company. To determine the business rules, you must first create a performance-based framework, where employees are both objectively and subjectively measured.

Budgeting for these programs is similar to sales forecasting — to be successful, you must be able to predict employee performance in relation to the program’s business rules.

Distributing a Budget

Organizations allocate budget to a budget holder — a division, vice president, location or manager — based on a variety of criteria. Typically, budgets are distributed in one lump sum, in one of the following ways:

- Flat amount: Each budget holder is given a flat amount determined by the budget controller

- Equal amount: Each budget holder is given an equal amount regardless of headcount, again determined by the budget controller

- Per employee: A predetermined amount is issued per employee to the budget holder to ensure every employee gets something

- % of payroll: Funds are distributed to budget holders based on the % of payroll they represent

Types of Points-Based Employee Recognition Programs

There are many types of programs that can be designed to communicate and help administer the earning of points. Program rules should be designed to drive specific behaviors — such as achieving specific goals, or exhibiting behaviors — and values should be assigned appropriately for each category or criteria. This will help the issuer control their budget and understand a best-practice reward value. By doing so, the issuer is guided towards rewarding the behaviors identified for that particular program. When employees see they are being rewarded for specific actions, it reinforces those behaviors, long-term.

Here are a few examples of typical Points-Based Employee Recognition Programs:

- Spot Programs are designed for ongoing use by budget holders or Managers to recognize employees. These programs reward employees with valuable points for positive behaviors or criteria with specific levels of awards tied to those efforts.

- Nomination Programs are typically designed for peer-to-peer nominations. Employees can recognize their peers by nominating them for awards. Budget holders or managers approve nominations and award points based on positive behavior.

- Special Programs are designed for single, multiple, or ad-hoc programs, contests, or discretionary campaigns that are tracked and managed internally.

- Award Codes give a manager a way to instantly recognize, in person, an observed behavior with a physical recognition card, which contains information to transfer points to the employee’s personal point bank.

Using and Redeeming Points

Point Set Up

When determining the value of a point, it's important to not just arbitrarily set a dollar-to-point conversion. The conversion should make sense. Long gone are the days when convoluted equations were created to hide the value of overpriced awards, as employees deserve transparency and are savvy consumers.

Typically, point values can be set up in a variety of ways. For example:

1 point = $1

1 point = $.01

1 point = $.005

While not trying to hide the value of a point, using a penny or half-cent points takes the focus off the monetary value of the award and more on the aspirational and emotional aspects of the award. Additionally, penny points allow employees to easily include any applicable shipping and sales tax when redeeming that they might not get with dollar points.

Employees see points deposited into their online, personal point bank. As points are distributed and redeemed, their point balance is displayed. Depending on how your program is set up, points can accumulate and be combined from any point program.

Point Distribution

The success of a points-based program hinges on two critical activities: point issuance and point redemption. Managers can make one of the largest impacts on engagement with simple recognition and point issuance — make sure there are multiple opportunities for recognition, the rules defined and the goals attainable.

When distributing budgets, make sure you are putting them in the hands of those who can most directly observe, measure, and reward those who deserve recognition.

Without point redemptions, you only use half of the recognition opportunity:

- Until a reward is redeemed, employees are much less likely to repeat the behavior that earned them that reward

- Encourage more recognition to build accounts for those who are working towards an aspirational item

- Promote redemption through communications and openly celebrating individual achievements

Redeeming Points

Points are typically redeemed for gift choices that include merchant gift cards, open loop gift cards (Mastercard and Visa), charitable donations, and merchandise (jewelry, watches, computers, electronics, health and beauty, home and garden, luggage, sports and lifestyle, toys, tools, and more). Award choices should be carefully considered and reflect the different segments of your workforce. Additionally, to help drive the performance of your program, award choices should include current, popular, and high-quality gift selections that your employees would aspire to obtain.

Redemption

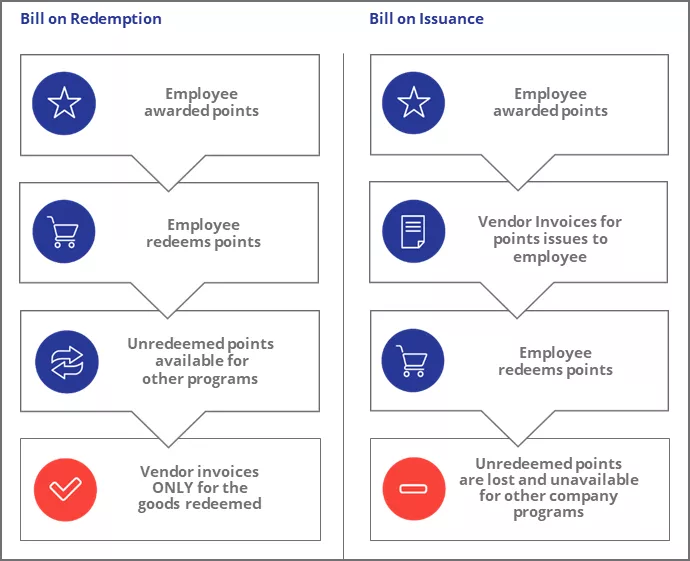

Bill on Redemption vs. Bill on Issuance

Bill on Redemption

- Pros: Allows a company to only pay for awards selected

- Cons: Points “banked” create an accounting liability if allowed to never expire

Bill on Issuance

- Pros: Alleviates accounting liability for unused points

- Cons: Points that may never get used are unnecessarily paid for

Accruing Awards

Most programs, including those operated by Inspirus, allow employees to accrue points over the life of the program with no expiration because of it:

- Motivates employees; expiring points may demotivate employees because they were unable to fulfill their recognition experience

- Gives the employee the ability to “bank” points to build towards an aspirational item

- Gives the employer a chance to reclaim former employees’ unused points if they had not been taxed

Expiring Points (Non-accruing Awards)

If your organization chooses to expire points, be sure to give plenty of notice and encourage redemption. Companies who allow points to expire may elect to account for the unredeemed points as an accrued liability:

- Accrued liabilities are amounts you owe in the future that are included on your business balance sheet

- Gives accounting and management full exposure to the financial potential of unredeemed points

- e.g. When reward points are issued from a “manager” to a “recipient,” this is an expense that has incurred, but can’t be considered paid until the “recipient” redeems his or her points.

Tax Implications

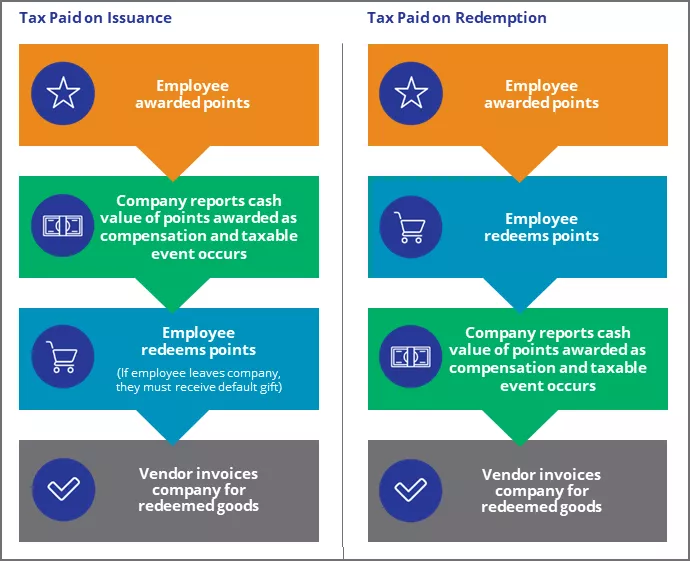

Tax Paid on Issuance vs. Tax Paid on Redemption

Pax Paid on Issuance

- Pros: Covers a company on all tax liability

- Cons: Employee gets taxed even if they never redeem points; it's harder to recoup unused points

Tax Paid on Redemption

- Pros: Minimizes the tax burden to only awards they physically receive; Nothing owed to former employees; may recoup unused points.

- Cons: May complicate taxation reporting

Grossing Up Taxes

Most employers “gross up” the awards to alleviate additional tax burdens on their employees. Fair market value calculations are used to reduce the taxable value of the award to the employee and therefore reduce the amount spent on gross-up:

- e.g. Cost of the award (paid to the vendor for the award) x 65% = Fair Market Value (FMV)

- e.g. $100 award is calculated at $65 FMV ($100 x 65%). The gross-up is calculated at 45% of $65 or $29.25. (Instead of 45% of $100 or $45)

Or, the company may decide on a fixed gross-up percentage such as the supplemental tax rate or 28%, 35%, or some other arbitrary figure that the company feels it can afford to offset the taxes associated with the award.

Recognition programs motivate employees to perform at their very best, increase job satisfaction, and contribute to higher retention rates. Points-based systems — similar to credit card loyalty programs — are one option that is comfortable for employees to use and easy for employers to implement.

Related articles